The day you sell your first course in Austria, you also join a club you never asked to join: VAT payers. It sounds heavier than it is. Once you know which rate applies, when you actually have to register, and how cross-border sales work, Austrian VAT on online courses turns out to be fairly predictable — and mostly a setup job you do once.

Here’s the short version. In Austria, selling an online course is normally a taxable service at the standard 20% rate, even when the content is genuinely educational. Education is not automatically VAT-free. You only escape charging VAT if you stay under the small-business turnover limit, or if your course qualifies as officially recognised training — which most self-paced courses and coaching don’t. This guide walks you through the rates, the registration thresholds, selling across the EU, the education exemption, and how to translate all of it into a clean setup when you sell through Maatos.

A quick note before we start: this is general information, not tax advice. VAT rules change and their application depends on your exact situation. Check with a qualified tax advisor or the Austrian tax authorities before you make decisions — especially on the exemption question, where the details do the heavy lifting.

How VAT works in Austria, in plain terms

In Austria, VAT is called Umsatzsteuer (USt). It applies to most goods and services a business supplies while doing business. Sell a course — in a room, live online, or on demand — and that sale is generally taxable unless a specific exemption fits.

The system sits on top of EU law (mainly the EU VAT Directive, 2006/112/EC) but runs through national legislation, chiefly the Umsatzsteuergesetz (UStG). So the EU sets the frame and Austria decides how it plays out in practice, with the tax authority’s guidance filling in the gaps.

One principle matters more than any other for course creators: the Austrian tax office looks at the legal classification of what you’re selling, not at how educational it feels. Digital delivery, self-paced content and commercial training tend to land in the “taxable digital service” box. That’s the assumption to start from — then check whether an exemption genuinely applies to you, rather than hoping it does.

Which VAT rate applies to your course?

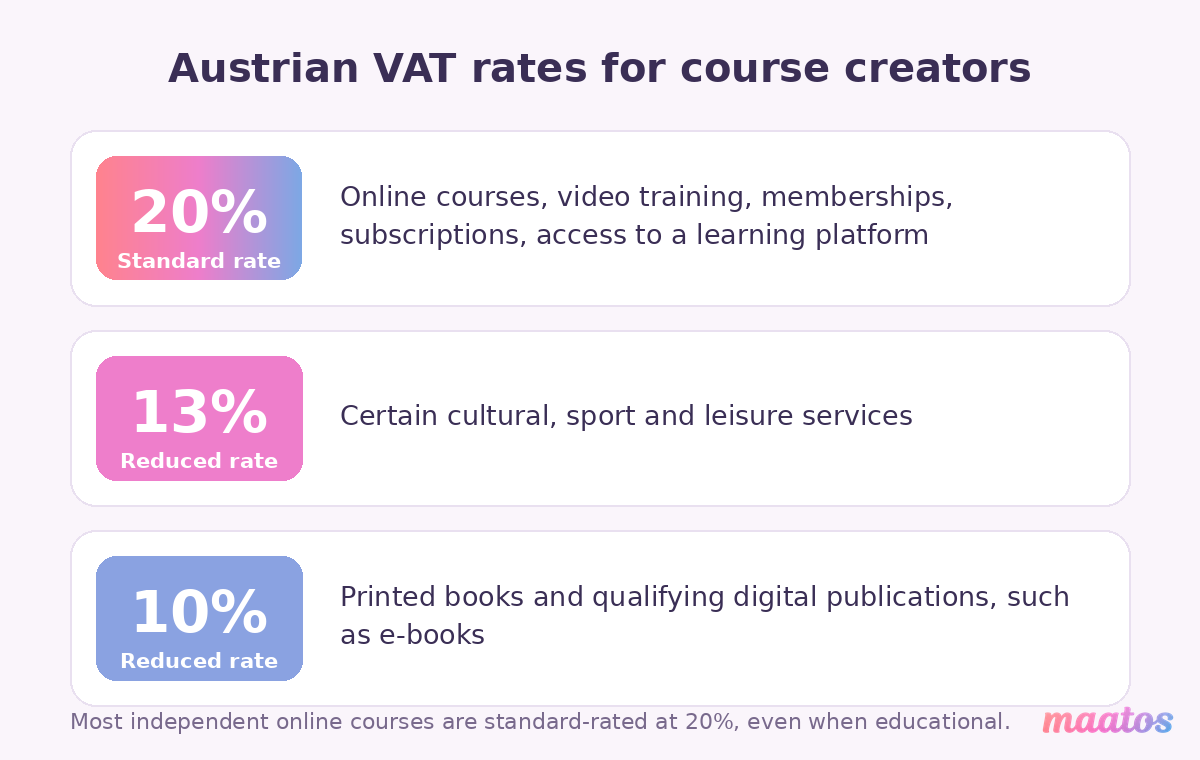

Austria has one standard rate and two reduced rates, and for most course creators only the first one is in play.

The standard rate is 20%. It covers the vast majority of services, and that includes online courses, video training, memberships, subscriptions and access to a digital learning platform. If your product is a course as most people picture it, assume 20%.

There are two reduced rates as well. 10% applies to certain essentials and cultural products — printed books, and qualifying digital publications such as e-books. 13% applies to a narrower set, mostly cultural, sporting and leisure services. Neither is a general “education” discount, and this is where people trip.

A course that includes video lessons, interactive modules, quizzes, coaching or a community is taxed at 20%, educational or not. The reduced 10% book rate doesn’t stretch to interactive or audiovisual learning. And if you sell a bundle — say, video lessons plus a PDF workbook — VAT law asks whether that’s one combined service or several separate supplies. In practice most online courses are treated as a single digital service and taxed entirely at the standard rate.

When do you actually have to register for VAT?

Whether you register depends on where your business is established and who your customers are.

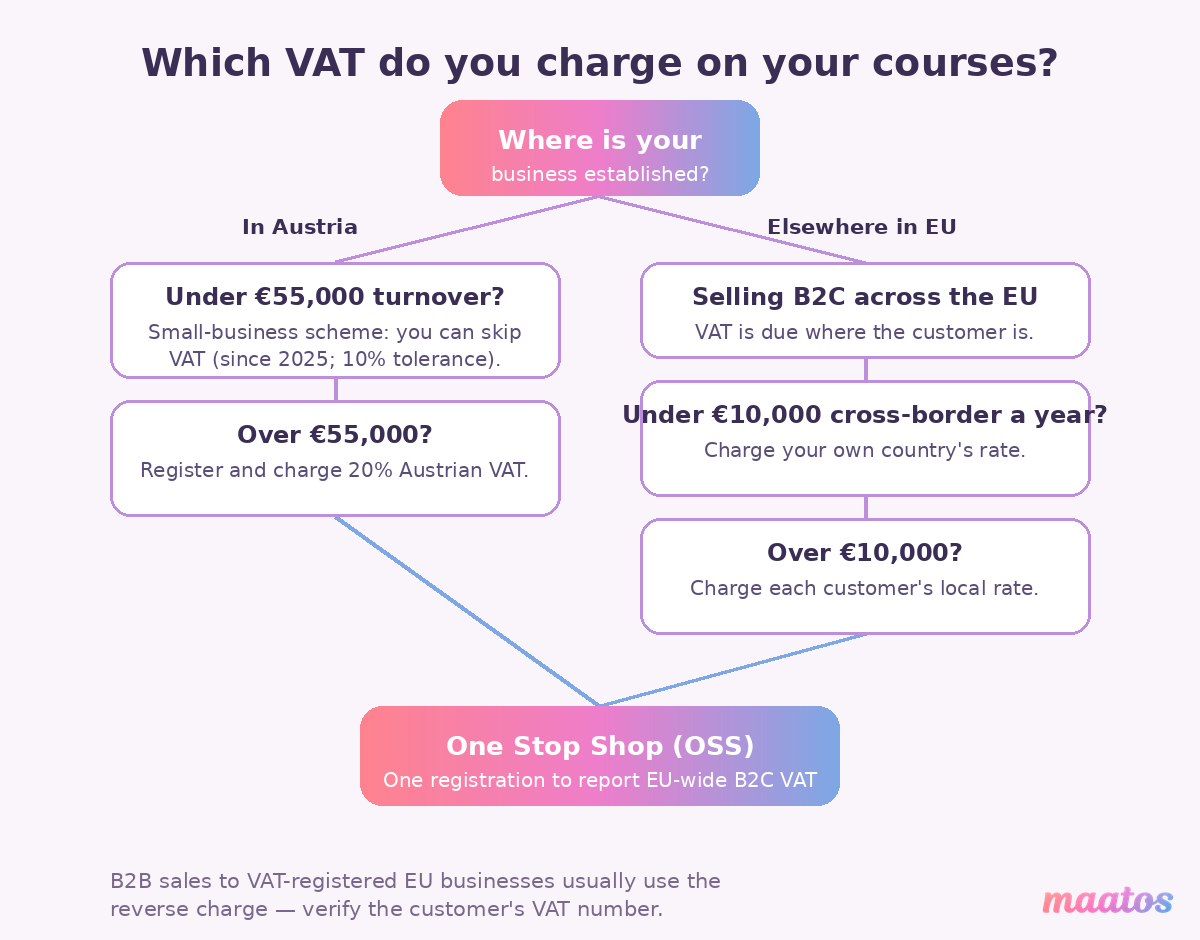

If your business is established in Austria, you may qualify for the Kleinunternehmerregelung, the small-business scheme. As of 1 January 2025 the limit rose to €55,000 in annual turnover (up from €35,000). Stay under it and you can choose not to charge VAT — simpler admin, but you also can’t reclaim VAT on your own business expenses. There’s a helpful cushion, too: a 10% tolerance rule means going over the limit by up to 10% in a year doesn’t cost you the exemption until the following calendar year, so a single good month won’t blindside you.

Cross the €55,000 line for real and registration becomes mandatory — you charge Austrian VAT on taxable sales from then on.

If your business is not established in Austria, there’s generally no registration threshold for taxable supplies made in Austria — in principle you’d register from the first taxable sale, unless an EU scheme covers you. (Since 1 January 2025 there’s also a newer EU-wide small-business exemption that can, under conditions, let a business established in another EU country use Austria’s small-business relief. It’s genuinely useful but the eligibility rules are specific, so treat it as “worth asking your advisor about,” not a given.)

For most creators selling to private customers across the EU, the practical answer is the One Stop Shop (OSS). Register once, and you report and pay VAT on all your EU consumer sales through that single registration instead of registering in each country separately.

There’s one more threshold that saves small sellers a lot of admin, and the original version of this guide skipped it. If your total cross-border B2C digital sales to other EU countries stay under €10,000 a year (net), you’re allowed to charge your own country’s VAT rather than the customer’s. Once you pass €10,000, you switch to charging the customer’s local rate — and that’s exactly the moment OSS earns its keep.

Selling across borders: business customers vs private customers

Cross-border sales are where the rules branch, and the split is simply about who’s buying.

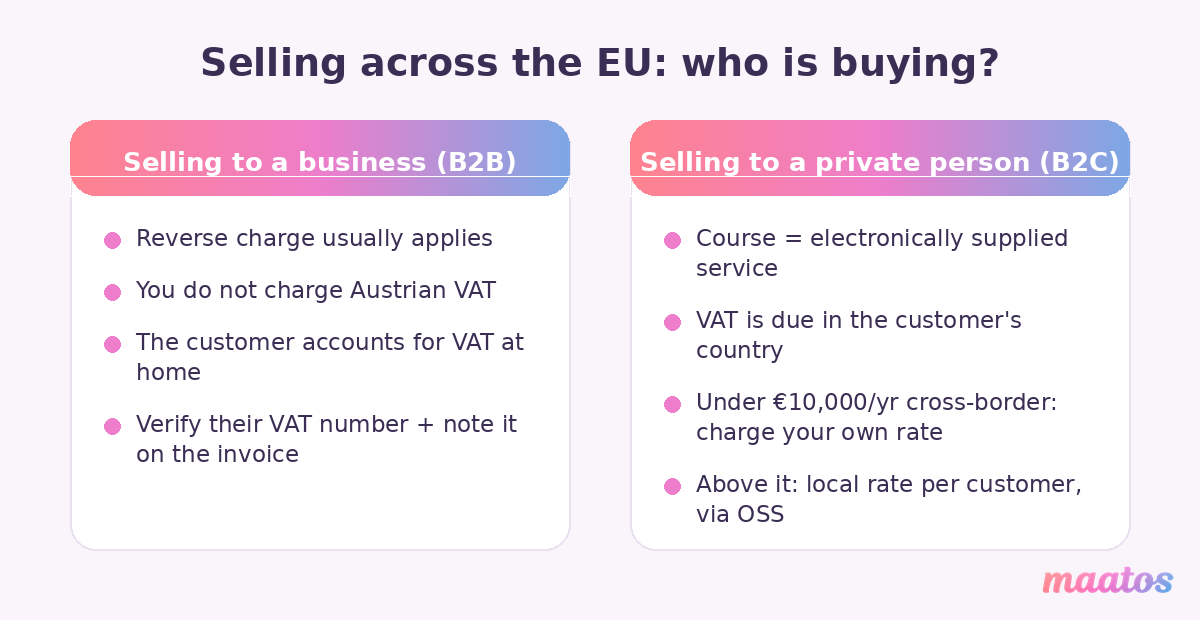

Selling to businesses in the EU (B2B)

When you sell a course to a VAT-registered business in another EU country, the reverse charge mechanism usually applies. You don’t charge Austrian VAT; the customer accounts for VAT in their own country instead. To do it properly, verify the customer’s VAT identification number and state clearly on the invoice that the reverse charge applies. Skip those two steps and you’ve got a paperwork problem later.

Selling to private customers in the EU (B2C)

For sales to private individuals in the EU, online courses count as electronically supplied services. Under EU rules, VAT is due where the customer is located, not where you are. So if you sell to learners in several EU countries, you may be applying several different VAT rates — France’s, Germany’s, Spain’s — depending on where each buyer sits. OSS lets you handle all of that centrally while still applying the correct local rate to each sale. (Below the €10,000 threshold above, you can keep charging Austrian VAT until you grow into the destination rules.)

Selling to customers outside the EU? EU VAT usually doesn’t apply, but local taxes or digital-service rules in the customer’s own country still might — the US, the UK and others each have their own approach. If a big share of your audience is British, our companion guide on selling online courses in the UK and VAT after Brexit covers what changed.

Is your course VAT-exempt as education?

Austria does exempt some educational services, but the exemption is strictly defined and widely misread.

Education can be VAT-exempt when it counts as recognised training or instruction delivered by an institution that meets specific legal and quality criteria — think formal education, vocational training, or courses from officially recognised institutions. For an independent creator or online educator, the exemption normally only applies if you hold official recognition or certification from a competent authority. Without it, the exemption doesn’t apply, however clearly educational or skill-building your content is.

This is the single most common misunderstanding. Teaching a professional skill, coaching, or selling a self-paced course does not automatically make it VAT-exempt. In practice, most independent online courses in Austria stay taxable at the standard 20%. If you think you might genuinely qualify, that’s a conversation to have with an advisor before you switch VAT off at checkout — not after.

What about e-books and digital publications?

Digital publications — e-books, digital manuals, online magazines — can qualify for the reduced 10% rate in Austria, but only if they meet strict criteria.

To qualify, the content has to be mostly text and work as the digital equivalent of a printed publication. Add meaningful interactivity, video, quizzes or coaching features and it generally falls out of the reduced rate and back to 20%. So if you sell digital publications alongside courses, keep them clearly separated in your catalogue, your checkout and your invoices. Fold a genuine e-book into an interactive course as one product and you can accidentally drag the whole sale up to the standard rate.

Other reliefs worth knowing about

Beyond the VAT exemption itself, a couple of Austrian reliefs are worth having on your radar.

From the learner’s side, certain education and training costs can be deductible as professional expenses under Austrian income tax rules. It doesn’t change your VAT obligations as the seller, but it can shape how you position a course to a professional audience — “this may be tax-deductible for you” is a fair, useful line when it’s true.

From the business side, the small-business scheme stays the most common relief for early-stage creators based in Austria. Choosing it is a strategic call, not just an admin one: it keeps VAT simple, but it blocks VAT recovery on your expenses and can dent your credibility with B2B clients who expect a VAT-compliant invoice. If you’re mostly selling to businesses, staying “small” on paper can quietly cost you.

Handling VAT for your courses in Maatos

Maatos is built for creators selling across borders, and clean VAT starts with correct configuration — the same point our broader guide on handling VAT and sales tax for digital courses makes.

A few things to get right inside your setup. Define where your business is established and whether you’re VAT-registered — that decides whether VAT is applied at checkout and which rates come into play. Categorise your products with care: courses, memberships and coaching access are normally digital services at the standard rate, and a digital publication should only be flagged as one if it truly meets the reduced-rate criteria. If you sell across the EU, pairing your Maatos store with OSS lets you apply the right local rate per customer while keeping your reporting in one place.

The nice part is what runs on its own. On Maatos, VAT is calculated automatically and invoices are sent to your customers without extra work from you, and you can accept payments through Stripe and Mollie — so the mechanical side of compliance mostly takes care of itself once it’s set up.

One honest limit: a platform can automate the calculation, but it can’t decide whether your specific course qualifies for an exemption. That legal judgement stays yours (and your advisor’s). Tools handle the sums; you own the classification.

Frequently asked questions

Do you charge VAT on online courses in Austria?

Usually yes. An online course is normally a taxable electronically supplied service at the standard 20% rate, even when it’s educational. You only skip VAT if you’re under the small-business turnover limit or your course is officially recognised, exempt training — which most self-paced courses and coaching are not.

What VAT rate applies to an online course in Austria?

The standard 20% rate. The reduced rates (10% for books and qualifying e-books, 13% for certain cultural, sport and leisure services) don’t cover interactive or video-based courses.

When do I have to register for VAT in Austria?

If your business is established in Austria, once your annual turnover passes the small-business limit of €55,000 (in force since 1 January 2025), with a 10% tolerance in the year you first exceed it. If you’re established elsewhere, there’s generally no threshold for taxable supplies in Austria — though OSS and the €10,000 EU-wide threshold usually shape what you actually do.

Is educational content automatically VAT-free in Austria?

No. Exemption is strictly defined and normally requires official recognition or certification from a competent authority. Teaching a skill or selling a course doesn’t qualify on its own, so most independent online courses stay standard-rated.

How do I handle VAT when I sell courses across the EU?

For private (B2C) customers, VAT is due in the customer’s country. Below €10,000 in total cross-border B2C digital sales a year you can charge your own country’s rate; above it, you charge each customer’s local rate and report everything through the One Stop Shop (OSS) on a single registration. For business (B2B) customers, the reverse charge usually applies — verify their VAT number and note it on the invoice.

Does the reduced 10% rate apply to my course if it includes a PDF or e-book?

Not usually. A standalone e-book that’s essentially text can qualify for 10%, but bundle it with interactive or video course content and the whole sale is generally treated as a single digital service at 20%. Keep genuine publications as separate products if you want the reduced rate to stick.

Can Maatos handle Austrian VAT for me?

Maatos calculates VAT automatically and sends invoices to your customers, and works with OSS for cross-border sales — so the calculations and paperwork are handled once you’ve configured your establishment, registration status and product types correctly. Deciding whether a course is exempt is still your call.

Getting it set up

Austrian VAT on online courses comes down to a handful of decisions you mostly make once: assume 20% unless you have a real reason not to, pick the right registration path for where you’re based, and set your products up so the correct rate is applied at checkout. Get those right and VAT stops being a worry and becomes background noise — which is exactly where it belongs while you focus on teaching.

If you’d rather not wire that up alone, that’s the whole point of the platform. Start your free trial and set up a course store with VAT and invoicing handled automatically — the first 30 days are free, and plans start at €49 per month (excl. VAT). Want to compare what each plan includes first? Take a look at pricing, or let our done-for-you service build the whole thing for you while you concentrate on the course itself.

Official sources and further reading

For the current rules straight from the source (and to double-check anything here against your own situation):

- Austrian Federal Ministry of Finance (BMF) — VAT overview: bmf.gv.at/en/topics/taxes/vat

- Austrian Business Service Portal (USP) — VAT in Austria: usp.gv.at — Umsatzsteuer overview

- USP — Austrian VAT rates and exemptions: rates and exemptions

- USP — small-business scheme (regulation since 1 January 2025): Kleinunternehmen

- European Commission — VAT rules for digital services: taxation-customs.ec.europa.eu/vat_en

- European Commission — the One Stop Shop (OSS): vat-one-stop-shop.ec.europa.eu

- EU “Your Europe” — cross-border VAT for business: electronically supplied services

Building the wider European picture? Start with our VAT overview for online courses across the European Union, then dig into the country you sell into most: Germany, France, Poland, Portugal, Croatia, Estonia, Finland, Hungary, Latvia, Malta, Slovenia or Bulgaria. For everything filed under selling, the selling courses hub collects it in one place.